The Next Great Insight™

The Next Great Insight™

Student loan forgiveness, private equity, and data-as-a-liability

Ranjan here. Today I'm going to talk about The Next Great Insight.

A disclaimer: While I have professional experience with currencies and debt, and personal investing experience with public equities, I have no real experience in private market investing. My entire knowledge of private equity consists of reading Dan Primack and Matt Levine’s newsletters.

But this is The Margins, and exploring ideas is why we spend time writing this newsletter. So here we go with an attempt at justifying the bombasity of the subject line.

Robert Smith’s Great Insight

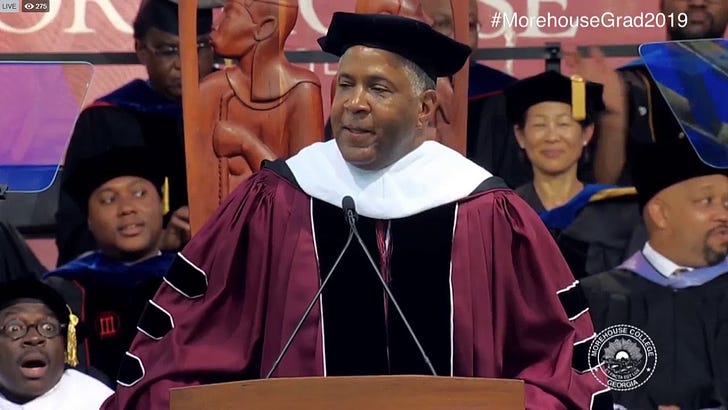

You all probably heard about the private equity guy who, while giving the commencement speech at Morehouse, announced he would be paying off the entire graduating class's student loans. I will refrain from communicating my thoughts on the action itself (though this NY Times editorial board piece captured it well), but it did make me very curious about the donor, Robert F. Smith.

I was speaking with a friend who works at a hedge fund that invests primarily in software companies, and he could not stop gushing about Vista Equity Partners, the private equity firm that made Robert F. Smith rich. He kept telling me about Smith's Great Insight.

This Forbes piece was the best thing I found that tells his whole strategic story, but let me try to do it justice:

Up until the 1990s, software cash flows were thought of as....just cash, no different than the dollar bills you would hand a cashier. Investors and lenders all wanted to see hard assets: factories, desks, physical inventory. Smith got two things very, very right.

We all know Andreessen made his money on software-is-eating-the-world, and so did Smith. He bet software would transition from nerdy, techie industry to an underlying operational tenet of the modern economy. This was the macro insight, but…

The even more genius innovation was realizing a cash flow resulting from a sticky software product was an incredible asset to be leveraged. There was a ton of locked-up value in the contract itself. It was so much more than just cash.

An underlying part of the thesis was (again from Forbes):

“Software contracts are better than first-lien debt,” Smith says. “You realize a company will not pay the interest payment on their first lien until after they pay their software maintenance or subscription fee. We get paid our money first. Who has the better credit? He can’t run his business without our software.”

As software became increasingly integral to the operational survival of a business, that contract became a lucrative asset, something that might be paid out even before interest on senior debt. Prior to Vista, banks wouldn't dream of lending against a software contract. The conventional wisdom was that, "a few innovative lines of code from a competitor could make a business obsolete overnight."

But most of our readers understand exactly how sticky enterprise software can be. Smith’s secret sauce was to convince banks to lend with the software cash flows as the underlying collateral. You then use that to invest back into the company on growth or acquisitions. It's classic private equity, but with an underlying asset that no one had ever noticed.

The Top-Secret Vista Playbook

The other half of the equation would also make an MBA strategy class swoon. Smith worked as a chemical engineer until 1992 when he went to Columbia Business School. From there he became a Goldman M&A banker. This combination of experience allowed him to understand that software companies, up until that time, were primarily of an engineering mentality. But, he had seen a few companies that truly excelled at optimizing the sales & marketing side of things, and felt there was a huge opportunity to translate their best practices across the industry (Forbes):

“Nobody ever taught these guys the blocking and tackling of running a software company"

Simple things like increasing renewal prices or charging for customer service requests just weren’t done. This led to a somewhat mythical best practices bible of sorts, with the lock and key held by Vista (Forbes):

To implement his playbook, Smith created an in-house McKinsey: Vista Consulting Group. These employees, now 100 strong, help portfolio companies implement the best practices, also 100 strong, most of which run three to ten pages, with reams of attachments and examples. Printed out, they fill binders. They are stored in a password-protected online library, available only to authorized portfolio company managers.

“I just had an employee get a promotion,” says Kristin Nimsger, CEO of Social Solutions, a cloud company providing data-management software for nonprofits like the United Way of Metro Chicago. “He was super-excited to get a log-in.”

My co-host Can checked in with a friend who had worked at a Vista-owned company, and they affirmed, people will even forego higher pay at other firms to remain in the treasured network.

This stuff seemed so simple, but Forbes, crystallizes the formula:

In isolation, many of the playbook’s best practices seem mundane. But software companies are often rife with eccentricities and legacy processes endemic to startup culture. Things like weekly deal-pipeline meetings, commonplace at B-school-driven corporations like IBM and Procter & Gamble, are often absent. By sticking to the rules in Smith’s playbook, his software companies are transformed. Add some modest leverage, and, voilà, Vista got amazing returns.

I love this whole story. In a world where Softbank’s Vision Fund wants to IPO itself, financial engineering can seem like smoke and mirrors. This is something that just makes so much damn sense. In fact, the first question I asked my friend was why didn't everyone replicate this right away? When I was discussing this post with Can, that was his exact first question. The best ideas usually are the ones that are annoying at how clear and obvious they are.

The Next Great Insight™

It's time to get a little wild. My conversation about Vista led to the natural, subsequent #FinanceBro conversation, "What is the next great insight?"

Here is my attempt at formulating an idea. As we've had more readers writing in, I would love any of your thoughts.

The two questions we need to answer:

What is a core piece of investing conventional wisdom that could radically shift?

What is something no one thinks of as an asset, that holds a ton of unlocked value?

This is The Margins, and we have been writing for weeks about data-as-a-liability, so let’s make that central.

DaaL

For the past few decades, the investing thesis has been “the more data, the better”. The more data you collect, the more value you can extract. We think this will shift. While the speed of the change is something that remains to be seen, the Data Risk Trifecta of policy regulation, consumer backlash, and cybersecurity risk all mean data practices of companies will have to be radically evolve.

But you can't just hit rewind. If you've built your entire company on a loose and dirty data mentality, you can't just rein things in. Pandora is out of the box. Facebook is enemy #1, but from tiny startups to big platforms, I would guess most companies have prioritized growth and data collection over data infrastructure and security. It would’ve been madness not to.

But some companies must’ve been building processes and infrastructure around a better collection and handling of data.

What if those data processes and infrastructure are the actual asset?

I know, it's a bit weird, but let me try 😀.

First, the defensive advantage.

The companies that viewed data infrastructure and processes as an asset to be built, rather than an expense to be managed, will be far better positioned in the coming decade. The data risk trifecta, defined above, feels inevitable. GDPR and CCPA are moving us into this world, cybersecurity-related lawsuits will become the norm and people will leave products that feel insecure. There will be costs.

The conventional viewpoint is that these are future costs to be managed, i.e. how do I lower the expected outlay of a data breach lawsuit? But that looks at risk management from a purely defensive lens. One of the things I learned in big-bank trading was, the better your risk management systems, the more value can be created. Better decisions are made, smarter risks are taken, and increased confidence is seen in everything you do.

Yes...I know big bank trading risk management systems don't have a great reputation, but seriously, I saw tiny risk systems changes create massive value. Building a more secure process in any context can result in value creation beyond simple error removal.

To bring it to my current life, we create newsletters for a number of clients. We use a software called Litmus that has a feature to validate hyperlinks. I look at that as a risk-reduction process. Not worrying about linking the wrong URL does a number of things beyond just not sending incorrect links. It allows us to spend more time on the content itself. It provides the confidence to get more creative. It improves our relationship with clients that leads to more projects.

It feels a bit obvious to write: improving processes can realize exponential benefits. But, especially with data, I think it will be real.

The Mantra of Better Data

Then to make a bigger stretch here, there is the whole "small data" or "better data” instead of big data line of thinking. I touched on this in last week's CCPA piece:

perhaps a company’s ability to handle their data will slowly become a competitive advantage. Not just in siphoning consumers away from irresponsible competitors with the promise of trust, but even in building smarter models that use “better data” rather than more data. Maybe that’s how the winners of the next twenty years will define themselves.

Maybe the companies that have built up usable, secure and focused datasets end up with the better AI models. They could certainly end up better leveraging their own data for business results. I've watched clients with an email list of a few, focused thousand extract far more monetary value than those with a few, random million. This also feels cliche to write, but it is a sea change in data mentality.

I loved this paragraph from a paper on cybersecurity during M&A due diligence. I also think the term "hygiene" does well to explain the mentality shift (emphasis mine):

The end result of all this is that, according to our study and others, there is a push among IT professionals to go beyond mere due diligence and move toward the use of real-time analytics and other cybersecurity best practices to monitor vendors’ systems.

The lesson here is constant vigilance, e.g., letting an initial process of cybersecurity due diligence be the first, and not the last, word in an ongoing proactive and comprehensive cybersecurity policy that promotes cyber hygiene along with the best practices essential for battling advanced threats. Such a policy should be widely disseminated and regularly vetted as part of an overarching enterprise risk management process, along with having an incident response plan in place that includes private and public information sharing mechanisms.

To sum up: Good data hygiene can create value far beyond just saving on legal costs. It can unlock unexpected value. It’s an asset that maybe is so good that one day banks lend against your dataset, allowing you to lever up your firm, if that’s your thing.

And then, alongside our readers, we figure out our Margins Best Data Practices™. And we build a network of companies that create unparalleled value. And finally, we use our amassed wealth to then forgive all U.S. student debt.

Happy almost Summer!

A Song / Video

I’m just going to remember the end of that show with this video, and not the actual finale.